- SAVU Realty Newsletter

- Posts

- SAVU Realty January 2026 Newsletter

SAVU Realty January 2026 Newsletter

Adam Taivalkoski

January 06, 2026

January is a great time to evaluate the market and look ahead. While winter activity is typically quieter, preparation and clear strategy remain important.

In this issue, we share practical guidance on preventing property fraud, maintaining current homeowner’s insurance coverage, and a brief overview of market conditions.

Don’t get your property sold without your permission!

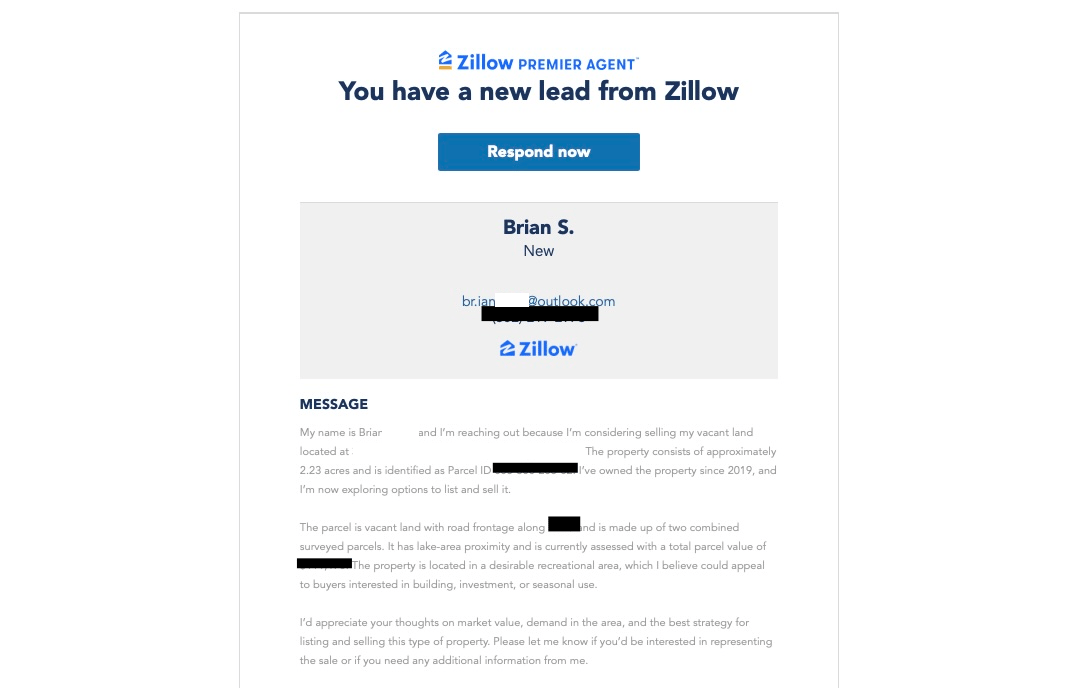

Property fraud is increasingly common with vacant land, seasonal homes, and properties owned by individuals who live out of the area. These properties are often targeted because they receive less day to day oversight, making fraudulent activity harder to detect.

Recently, I received a fraudulent email (see above) from an individual impersonating a property owner. The sender attempted to engage me to list a property, with the apparent goal of having proceeds wired to them under false pretenses.

Closer to home, a similar incident occurred in Calumet within the last quarter. An agent from outside of the area was hired to list a property and began fielding offers, only to later discover that the true owner had never authorized the sale.

The takeaway is straightforward. When you see a property listed for sale anywhere, you should not automatically assume the actual owner is the one behind the transaction. Without proper verification, buyers risk wiring funds to an unknown and potentially foreign party. The same caution applies to rental listings, where fraudulent postings are also common.

Insurance Coverage

Home insurance is essential for protecting your property, yet coverage lapses are common. Changes in billing, escrow adjustments, policy renewals, or lender requirements can create gaps if not monitored.

Homeowners should periodically review coverage limits and renewal dates, particularly when refinancing, changing insurers, or making improvements.

Ensuring premiums are paid on time and coverage aligns with replacement costs helps to prevent issues and protect both property and financial security.

If insurance has lapsed for a long period of time it can be difficult and cost extra to get a homeowners policy back in place.

If your home has $300,000 of replacement coverage, it could easily cost $500,000 to replace it. If your policy hasn’t been updated in a while, you could be underinsured if you were to have a total loss. This is especially true if your policy hasn’t been updated in the last 5 years due to dramatically higher labor and material rates.

You should also update your insurance company if a property has been changed to a rental or is vacant. Also, keep in mind that water damage isn’t covered under many policies unless you get the appropriate rider.

Market Overview

2025 resulted in positive trends with an increase of 6.8% more homes sold from 2024. Also, more liquidity in the local housing market has been beneficial for buyers as they have more options to consider.

Pricing trends also remained favorable for sellers. The median and average sales prices went up 11.9%.

Prices have gone up considerably, and so have the days on market. We are now seeing a typical home sell in 27 days versus 15 days. This gives buyers more time to think over an important buying decision.

From personal observation, the market remains very active right now. I am working with plenty of buyers who simply cannot buy until they find the right home. We are still in a seller’s market with not enough supply to meet demand. Based off of my interactions, I anticipate an even greater number of homes for buyers available in 2026. I also expect prices to continue to climb in 2026, though buyers should benefit from a broader range of available options.